Brazil's Generational Debt Trap: When Credit Comes Before Income

A 28-year-old social sciences student in Rio describes her financial life as a loop — pay down the card, run out of money, repeat [1]. Her situation, rather than accidental, is the product of a specific reversal of the slow and steady onboarding into the world of credit. The logical system where risk and access were roughly calibrated to each other has been replaced by one where income has less weight.

This change is not specific to developing economies like Brazil, where consumer credit culture has historically been more conservative and income-first. However, the results of Bolsa Família from 2003, and the market effects that Lula rode in his second term (2007-2011), meant that the availability of credit exploded post-2010. This was accompanied by a compressed technological shift, from LAN house to smartphone — a leapfrog pattern familiar across emerging markets. The mobile-first, credit-with-a-click approach, helped along by Nubank, PicPay and Pix, led to increased inclusion but also indebtedness.

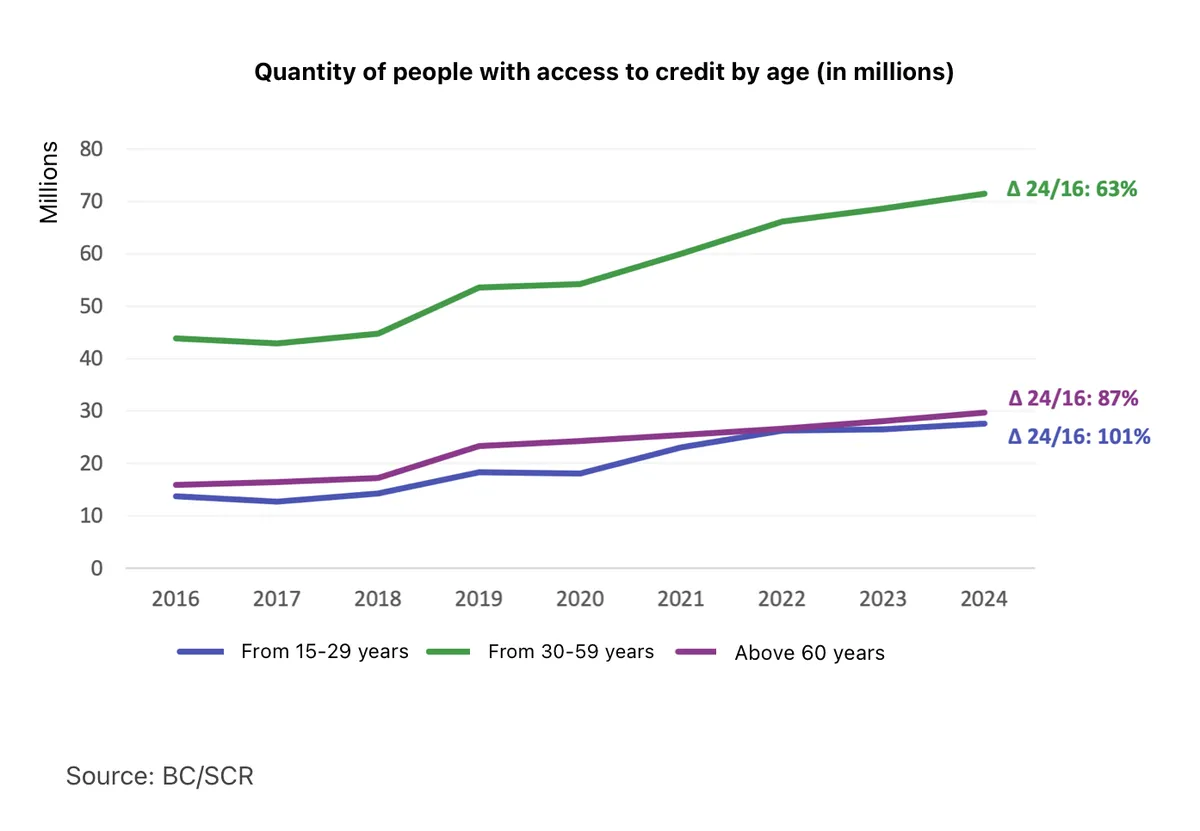

Brazilian fintechs under competitive pressure to acquire young customers early — that is, for their lifetime value — had little incentive for caution. The result: the number of people from 15-29 yrs old with active access to credit grew 101% between 2016 and 2024, according to Brazil’s Central Bank credit information system (SCR). The bulk of that growth occurred among those who earn up to two minimum salaries, which translates to roughly US$450–560 per month across the period [2].

That same SCR data from 2024 also shows structural risk, as young borrowers have been defaulting at higher rates (17.4% of those who are low-income) than adults and elderly across all income brackets. Credit cards were the most used product, with 17 million young Brazilians using them for one-time payments in 2024, while 79% simultaneously carried revolving credit or installments.

Easy fintech credit predisposes young borrowers to a psychological relationship with money that conflates access with security. For a cohort who tend to have lower emergency funds and exhibit riskier behavior, the perception of access to money rewards and reinforces their approach to anxiety management.

Luis Salvatore, president of Instituto Brasil Solidário, argues that young Brazilians are entering the financial system too soon and receiving financial education too late. The issue, he adds, is not merely a lack of information but a lack of formation for making decisions. [3]. The ease of the click of a button to access unearned funds together with the inability to understand the terms of repayment is a recipe for default and debt cycles, as well as damaged credit histories.

According to a 2023 OECD survey on adult financial literacy (analyzed by the Banco Central in 2025), Brazilians answered just over half of the questions correctly. The lowlights reflected questions on the calculation of simple interest (87% wrong), compound interest (53% wrong), and risk diversification (42% wrong).

This mathematical illiteracy compounds a type of psychological detachment that was already in play before the advent of fintechs. More specifically, a 2012 FGV study on the behavior role of credit card use by university students identifies a significant “loss of control” when physical currency is replaced by credit [4]. The use of a credit card makes the act of spending feel “intangible” compared to the physical exchange of cash and the transaction — which feels less “real” to the young consumer — directly facilitates a debt cycle. In the Brazilian context, credit is functioning as a “step to the unnecessary,” creating an illusion of abundance that encourages spending while hiding the consequences.

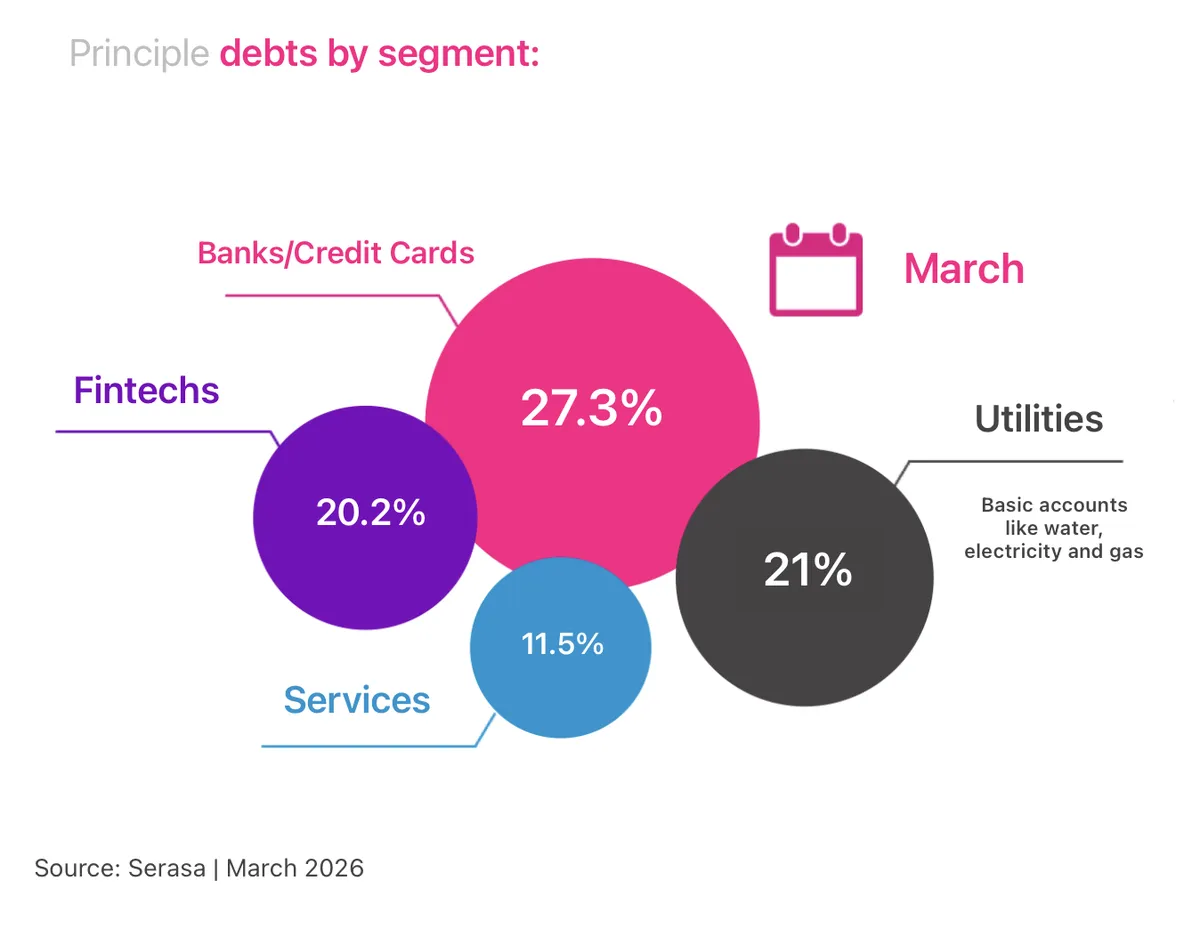

Today, the total number of Brazilians behind on payments exceeds 82 million — the worst level since 2012, when the FGV study was published. Young debtors between the ages of 18 and 25 make up 11.2% of the total, according to the latest Serasa figures from March 2026 [5]. Regardless, the question remains: is this sequencing reversal, where credit precedes income, solvable and, if so, by whom?

Lula's debt renegotiation program in 2023, known as Desenrola 1.0, provided relief for debt accumulated during the pandemic. It was a temporary patch: 9 million new defaulters emerged in the year after the program ended in May 2024. Under the government’s current answer to the problem, known as Desenrola 2.0, workers are able to withdraw up to 20% of their severance fund to pay debts [6]. The problem is that this response addresses symptoms rather than causes, by reducing the debt burden without touching the credit sequencing problem that created it.

Even with Desenrola 2.0, the can is still being kicked down the road. High basic interest rates, which are currently at 14.50% per year, together with limited financial education, will only lead to further editions of the same program. With nearly 30% of Brazilians’ income being consumed by debt payments, individual default rates can collectively turn into macroeconomic drag. Betting restrictions blocking debtors from online gambling for 12 months are yet another bandaid on a bucket with too many holes.

Sources

O Globo — Acesso a crédito dobra entre jovens e acende alerta sobre inadimplência precoce, May 3, 2026

Banco Central — Relatório de Cidadania Financeira 2025, including data drawn from the OECD/INFE 2023 Adult Financial Literacy Survey

InfoMoney — Jovens e endividados: falta de preparo aumenta dívidas entre jovens, mostra BC, April 15, 2026

FGV EAESP — O Papel do Cartão de Crédito no Comportamento de Compra dos Jovens Universitários, 2012

Serasa — Mapa da Inadimplência e Negociação de Dívidas no Brasil, March, 2026

Folha de Pernambuco — Desenrola 2.0 tenta alcançar classe média: endividados terão alívio até a eleição?, May 5, 2026